Lately, I’ve been getting quite a few questions from

homebuyers about the major changes to Fannie

Mae (FNMA). For starters,

allow me to define Fannie Mae: Fannie Mae is a government-sponsored enterprise

that primarily buys mortgages from lenders for cash or pools them and sells

them as mortgage-backed securities to investors on the open market.

So what’s changing about FNMA? Like most industries, nothing stays the same for long—and

real estate is no exception. There

are many changes coming along that will affect homebuyers in 2014 and one of

those is a new FNMA rule with gift down payments.

In the past, most homebuyers have not had the opportunity

to use 100% “gift

funds” (a financial gift from a spouse or other blood relative, even

one’s employer) for their down payment.

So many used the 3% down Conventional (97 LTV) or 3.5% down FHA option,

100% gift (96.5 LTV) options when purchasing a home or they would use a

conventional loan with 5% down. But because of major changes to the real estate

market, FNMA is now allowing homebuyers to use gift funds to make their 5% down

payment on a conventional loan, making the 5% (95 LTV) option much more

attainable, particularly for first-time home buyers.

So what does this mean for homebuyers exactly? A whole lot of opportunity. In order to get an understanding of this

change, I talked with Jim Griffiths, a Mortgage Advisor at Stonegate

Mortgage.

“There really is no downside to this change for borrowers,”

explains Jim. “While the 3% down

option went away, this allows more home buyers access to conventional lending programs. It’s

perfect for first-time homebuyers who may not have had enough time to save up

enough of their own cash reserves to make a down payment. They can really use this to their

advantage.”

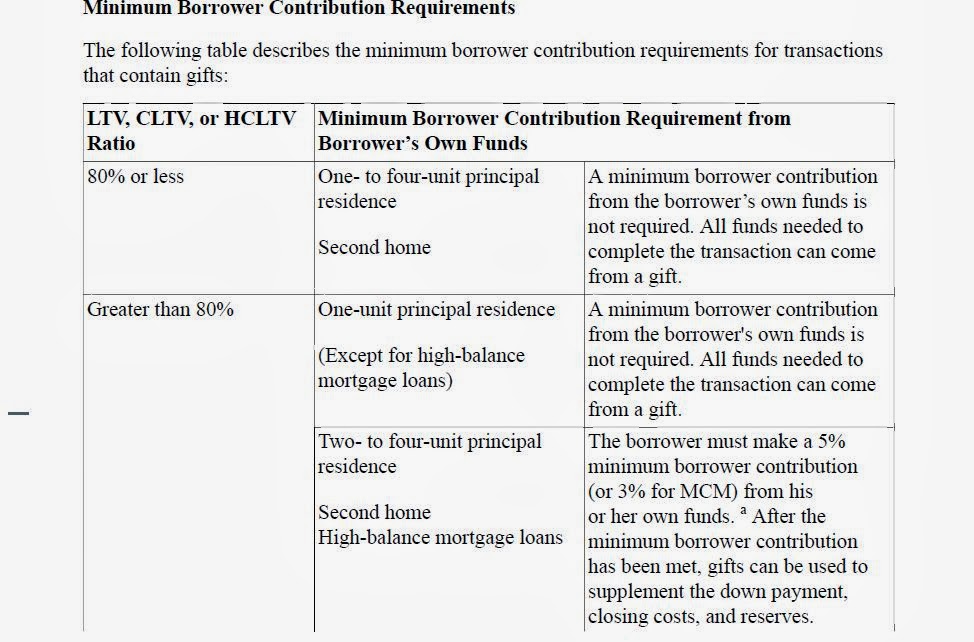

The table below will help homebuyers further understand this

change and see the minimum borrower contribution requirements for transactions

that contain gifts:

As Griffiths stated, with this

change, homebuyers are putting more skin in the game, not to mention more

investment in the market. The

message here is that investors want to see more “skin in the game” even though

it may be 100% gifted funds.

“Bottom line, if someone can help you with

your 5% down payment, you now have that option,” says Griffiths. “Conventional lending provides a much

less expensive option from a mortgage insurance perspective, which lowers the

overall monthly payment. In the

long run, it can also be cheaper than an FHA loan. My recommendation is that if

it’s available, take advantage of it.”

If you would like to take advantage of this new loan opportunity and begin the home buying process, please contact me today to schedule a private consultation.

Phone: 913.568.7355

Email: tohlde@kw.com

Website: www.toddohlde.com

Or, if you have more questions regarding the new Fannie Mae guides, or if you want to inquire about qualifying for a home loan, please contact Jim Griffiths:

Phone: 913.951.3786

Email: jgriffiths@stonegatemtg.com

Want more tips and breaking

news about the housing market? Stay posted on my Facebook page or contact me.